County Seat Newspaper

of Clare County

Harrison, MI

Harrison, MILight Rain and Breezy, 47°

Wind: 21.9 mph, W

Harrison, MI

During the upcoming August 4, 2020 Primary Election, Clare County and MSU Extension (MSUE) are asking the voters of Clare County to consider new millages, Clare County to support Animal Control Services (0.3000 mills) and MSU Extension to support MSUE Services (0.13000 mills). This will result in property taxes of $0.30 and $0.13, respectfully, per $1,000 of Taxable Value. These relatively small investments will serve the residents of Clare County in these areas if approved by the voter on Aug. 4.

The reason for this communication is to clarify the State required language on the ballot which unfortunately can be somewhat misleading or at least confusing. The ballot indicates within the language for these new millages in part that “If approved and levied, a portion of the millage monies raised in their respective jurisdictions may also be captured by the Downtown Development and Brownfield Authorities of the Cities of Clare and Harrison, The Downtown Development Authority of the Village of Farwell, the Village of Farwell/Surrey Township Local Development Finance Authority, and the Clare County Land Bank Authority pursuant to State Law.”

The fact is that this sentence only applies to the property taxes collected on the properties that are physically located within the Downtown Development Authority districts in Downtown Clare and Downtown Harrison and the Village of Farwell; the Local Development Finance Authority Districts in the Village of Farwell and the City of Clare; and the Brownfield Redevelopment Districts within the Cities of Clare and Harrison. All property taxes collected for these new millages on properties outside of these very small districts would be disbursed in their entirety to and used by the Animal Control facility and the MSU Extension Service. Only a very small portion of the taxes collected in these small districts are captured and disbursed to the DDAs/LDFAs/Brownfield’s, etc.

Furthermore, only a very small portion of the property taxes collected on properties that are physically located within these DDA, LDFA and Brownfield Districts is captured and thereby used by these authorities for authorized redevelopment programs. For instance, the Clare DDA District encompasses a very small area centered along McEwan and Fifth Streets in Downtown Clare.

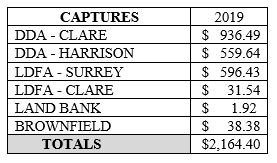

A 2019 millage example: The Clare County Transit Authority millage already in place in 2019 was at 0.3000 mills. For the 2019 tax year, the total tax levy to collect for Transit was $323,000. Of this $323,000 only $2,165 was capture in totality. That is less than 1%. See Graph for the breakdown.

Though understandable it is unfortunate that the prescribed and required ballot language does not specifically identify that the DDA/LDFA/Brownfield disclosure only applies to a very few properties located in very small, defined areas within Clare County. We encourage residents and property owners who may have questions or concerns, particularly on complex or confusing issues, to contact your elected and appointed government officials so that complete answers can be obtained.

Steve Kingsbury, MBA, CPFA, MiCPT

Treasurer, Finance and Technology Director, City of Clare

Jenny Beemer-Fritzinger, MBA, CPFIM, Clare County Treasurer

Comments

No comments on this item Please log in to comment by clicking here